A story is recently making the rounds on Yahoo! Finance regarding "new" collection agency tactics that focus on "customer service" and "friendliness."

According to reports published by the Association of Credit and Collection Professionals International (ACAI), the debt collection industry took in approximately $52 billion in revenue in 2013, compared $55 billion in 2010. That is "billions" with a "B:" i.e., a whole lot of money.

Though the industry may be attempting to rebrand itself based on a new-found commitment to "customer service," it is important to remember that debt collectors have one ultimate objective in mind: to get money from consumers.

Regardless of how friendly the letters may be, or how nice someone may speak to a consumer on the phone, debt collectors may still be hurting a person's credit, and they may be preparing to file a lawsuit against them. Moreover, if they choose not to sue, they may decide to sell the debt off to another collector who may not care so much about "friendliness."

Consumers would do well to remember that debt collectors are still required to play by the rules provided by the FDCPA, including: warning you that they are a debt collector attempting to collect a debt; debt validation letters; and refraining from unfair or abusive behavior. If a debt collector fails to do these things, even if they have a smile on their face, it is still a violation of the law.

Thursday, August 28, 2014

Wednesday, July 30, 2014

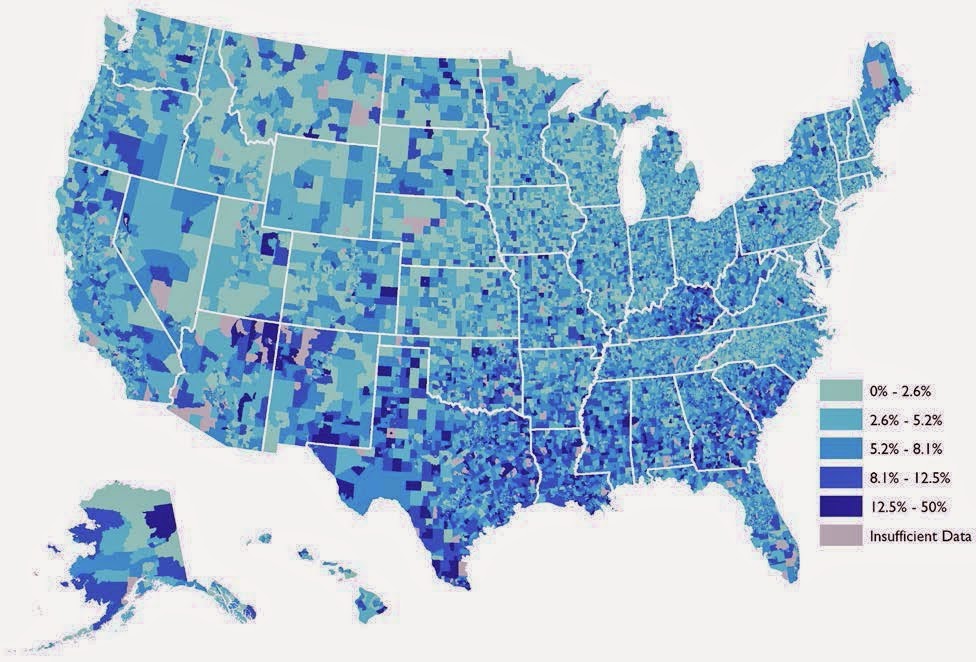

Study Says 35% of Americans Facing Collection Agencies

According to a recent study released by the Urban Institute, more than 35% of Americans have debts and unpaid bills that have been reported to collection agencies. These adults owe an average of $5,178.00. The full study can be found here.

The study reveals that the East South Central census region (which includes Kentucky) has the second-highest percentage of people with a debt in collections, with 41.3% of people having an account in collections.

Debt collectors do not just collect unpaid credit cards, but a wide-range of debts such as:

- MEDICAL

- cell phones

- utilities

- gym memberships

- book clubs

Every case is different, but many people facing debt collectors ultimately end up filing bankruptcy as a way to protect themselves, and to begin the process of rebuilding their credit.

Saturday, June 15, 2013

Debt Collectors and Original Creditors - What Law Applies?

This post aims to give you a general answer to this very common question. In general, the Fair Debt Collection Practices Act (FDCPA) protects

consumers from a wide range of abusive, harassing and misleading actions by debt collectors.

As its name implies, the FDPCA generally applies only to “debt

collectors” and not to original creditors.

Therefore, if you have a credit card from a company such as Capital One,

and Capital One calls you at midnight trying to collect the debt (which is not

allowed by the FDCPA), Capital One would most likely not subject to the FDCPA

because they are the original creditor.

On the other hand, if John Smith Collection Company called you at

midnight, trying to collect the Capital One debt, John Smith Collection Company

most likely would be subject to the FDCPA, because they are a debt collector.

Just because the FDCPA doesn’t cover original creditors,

doesn’t mean that original creditors can do anything that they want to try to collect from consumers. Many states have laws aimed at protecting

consumers from original creditors. In

Kentucky, this law is called the Kentucky Consumer Protection Act (KRS §

367.110), and it protects consumers from "unfair, false, misleading or deceptive acts or practices in the conduct of any trade or commerce." KRS § 367.170.

If you feel that you are being harassed by debt collectors

or original creditors, you should review your rights under the FDCPA and the

Kentucky Consumer Protection Act to determine whether they are violating the

law.

Subscribe to:

Posts (Atom)